This content is restricted to subscribers

Study: AVMetrics New Testing Methodology

This content is restricted to subscribers

AVMs React to New Final AVM Rules

On August 16th, Jon Wierks from First American penned an article about how First American is reacting to the new AVM Final Ruling. The article made several interesting points:

1. First American has specifically enhanced its AVM, their testing, and some of their tools in anticipation of the new rules. For example, FA has invested in explainable AI (xAI) in order to address fairness concerns.

Newer AVMs, like our Procision™ AVM Suite, were designed to comply with current AVM guidelines and in anticipation of the new guidelines.

2. First American expects AVM users to be expected to take on their own testing responsibility, and this doesn’t just apply to banks.

…new guidelines, Quality Control Standards for Automated Valuation Models, requires mortgage originators and secondary market issuers “to maintain policies, practices, procedures, and control systems to ensure that automated valuation models used in these transactions adhere to quality control standards

3. AEI’s recent AVM study has drawn attention to the biggest issues with AVM testing, and our new testing techniques are advancing testing beyond any other innovation in a decade.

For several years, AVMetrics has been developing a blind testing system that it will roll out later this year. Rather than sending the same addresses to various providers each month and getting back their valuations, AVM providers will now value every property in the U.S. — more than 100 million valuations each month — and send this data to AVMetrics. The testing company will ingest this data and then blind test it against future sales and listing prices as they transact. As you would expect, this is a massive undertaking for AVM vendors and AVMetrics, but it will separate the AVMs that test well from those that actually perform well in real-world conditions.

Wierks’ conclusions are right on target with our beliefs that improving AVM accuracy, precision and confidence scoring are making them more useful to industry, and that appropriate testing is a prerequisite to their widespread adoption.

#1 AVM in Each County Updated for Q2 2024

Every quarter we analyze all the top AVMs and compile the results. Click on this GIF to see the top AVM in each county for each quarter. As you watch the quarters change, you can see that the colors representing the top honors change frequently.

The main point is how frequently AVM performance changes. That should be no surprise, since market conditions change and AVM’s have different strengths and tendencies. Phoenix has more tract housing, and some AVMs are optimized for that. Cities in the northeast have more row housing, and some models are better there. But AVMs also change – a lot. Whole new models are introduced, but every model is constantly being improved as builders add new data feeds and use new techniques to get better results (with respect to new techniques, over at the AVMNews, we curate articles about AVMs, and we highlight several hundred new research articles about AVMs every year).

Q2 Change Highlights

As ever, if you watch a part of the map, you’ll see several changes. In Q2, we saw a changing of the guard. Here are some places to watch:

- In Texas, most counties changed leadership. The counties that include Austin and its suburbs changed leadership. Not Dallas, but most of the counties around Dallas, and not Houston (Harris), but most of the counties around Harris County changed leadership.

- Much of Alaska, and the West Coast changed leadership.

- Some less-populated areas had almost wholesale changes, such as Colorado, Nevada, New Mexico, the Dakotas, rural Michigan, Illinois, Missouris, Arkansas, Louisiana, Mississippi and more.

Takeaways

- Things change – a lot. Don’t rely on the results from last year. Heck, you can’t even trust last quarter! We compile these results quarterly, but our testing is non-stop, and we can produce new optimizations monthly based on a rolling 3 months or any other time period. Often, 3 months’ of data are required to get a large enough sample in smaller regions, but we can slice it every way imaginable.

- Use more than one AVM. It’s not obvious from a map showing just one AVM in each county, but if you think about what’s going on to produce these results, you’ll realize that AVMs are climbing all over each other to get to the top of the ranking. So, when you’re valuing a particular property, you just don’t know if it will be a good candidate for even the best AVM. When that AVM produces a result with low confidence, there’s a very good chance that another AVM will produce a reasonable estimate. Why not be able to take three, four or five bites at the apple?

#1 AVM in Each County Updated for Q1 2024

Every quarter we analyze all the top AVMs and compile the results. Click on this GIF to see the top AVM in each county for each quarter. As you watch the quarters change, you can see that the colors representing the top honors change frequently.

The main point is how frequently AVM performance changes. That should be no surprise, since market conditions change and AVM’s have different strengths and tendencies. Phoenix has more tract housing, and some AVMs are optimized for that. Cities in the northeast have more row housing, and some models are better there. But AVMs also change – a lot. Whole new models are introduced, but every model is constantly being improved as builders add new data feeds and use new techniques to get better results (with respect to new techniques, over at the AVMNews, we curate articles about AVMs, and we highlight several hundred new research articles about AVMs every year).

Q1 Change Highlights

As ever, if you watch a part of the map, you’ll see several changes. In Q1, markets continued to grind along with higher interest rates. We saw a changing of the guard. Here are some places to watch:

- In Texas, most counties changed leadership. The counties that include Austin and its suburbs changed leadership. Not Dallas, but most of the counties around Dallas, and not Houston (Harris), but most of the counties around Harris County changed leadership.

- Much of rural California, Oregon and Washington changed leadership.

- Some less-populated areas had almost wholesale changes, such as Colorado, Nevada, New Mexico, the Dakotas, rural Michigan, Illinois, Missouris, Arkansas, Louisiana, Mississippi and more.

Takeaways

- Things change – a lot. Don’t rely on the results from last year. Heck, you can’t even trust last quarter! We compile these results quarterly, but our testing is non-stop, and we can produce new optimizations monthly based on a rolling 3 months or any other time period. Often, 3 months’ of data are required to get a large enough sample in smaller regions, but we can slice it every way imaginable.

- Use more than one AVM. It’s not obvious from a map showing just one AVM in each county, but if you think about what’s going on to produce these results, you’ll realize that AVMs are climbing all over each other to get to the top of the ranking. So, when you’re valuing a particular property, you just don’t know if it will be a good candidate for even the best AVM. When that AVM produces a result with low confidence, there’s a very good chance that another AVM will produce a reasonable estimate. Why not be able to take three, four or five bites at the apple?

Why Mark Sennott’s Whitepaper Stopped Us Cold

At AVMetrics, we have to admit having mixed feelings about Mark Sennott’s recent whitepaper on AVMs. We’re quite grateful for his praise on our testing, which he describes as “robust, methodical and truly independent.” He echoes some of our key concerns:

- AVMs perform very differently, so it is important to test before using

- AVM performance changes more frequently than you’d think

- Everyone should employ a cascade using multiple AVMs, because it dramatically increases the accuracy of the delivered results.

However, there was something quite disconcerting in Mark’s telling of how AVMs are being used. In Mark’s words:

In practice, however, the top performing AVMs, based on independent testing performed by companies like AVMetrics, are not always the ones being delivered to lenders. The reason: self-interest on the part of the AVM delivery platforms who also sell and promote their own AVMs.

This very troubling delta between posture and operating practice had to be confronted first-hand by one of the lenders for which I provide guidance. What at first blush appeared as a straightforward exercise for the lender in vetting a platform provider’s cascade against AVMetrics independent testing results, became a ponderous journey to overcome contractual headwinds against a simple assurance the provider would indeed provide the highest scoring AVM model per AVMetrics recommendations. This was not the first time I experienced this apparent conflict of interest.

Kudos to Mark for writing openly about a practice that many in the industry would probably prefer that he kept quiet about.

AVMetrics Responds to FHFA on New Appraisal Practices

FHFA, the oversight agency for Fannie Mae and Freddie Mac, published a Request for Input on December 28, 2020. The RFI covered Appraisal-Related Policies, Practices and Processes. AVMetrics put forth a response including several pages and several exhibits making the case for using AVMs responsibly and effectively in a Model Preference Table®. Here is the Executive Summary:

The lynchpin to many of the appraisal alternatives is an Automated Valuation Model, a subject which AVMetrics has studied assiduously and relentlessly for more than 15 years. We point out that even an excellent AVM can be improved by the use of a Model Preference Table. MPTs enable better accuracy, fewer “no hits” and fewer overvaluations.

We also suggest an escalated focus on AVM testing, and we use our own research and citations of OCC Interagency Guidelines to emphasize the importance of testing to effectively use AVMs. We suggest that an “FSD Analysis” like the one we describe reduces risk by avoiding higher risk circumstances for using an AVM.

We suggest that the implementation of a universal MPT by the Enterprises will improve the collateral tools available and reduce the risk of manipulation by lenders. We also believe that a universal MPT can help redeploy appraisers to their highest and best use: the qualitative aspects of appraisal work. Our suggestion is that the GSEs endeavor to make the increased use of AVMs a benefit to appraisers, increasing their value-added and bringing them along in the transition.

AVMetrics’ full response is available here:

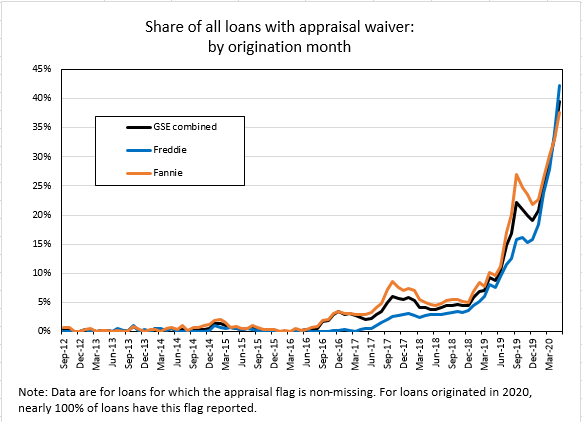

Property Inspection Waivers Took Off After the Pandemic Set In

Appraisals are the gold standard when it comes to valuing residential real estate, but they aren’t always necessary. They’re expensive and time-consuming, and in the era of COVID-19, they’re inconvenient. What’s the alternative?

Well, Fannie and Freddie implemented a “Property Inspection Waiver” (PIW) alternative more than a decade ago. However, it’s been slow to catch on.

But now, maybe the tipping point has arrived during the pandemic. Recently published data by Fannie and Freddie show approximately 33% of properties were valued without a traditional appraisal! (Most, if not all, would have used an AVM as part of the appraisal waiver process.) Ed Pinto at AEI’s Housing Center calls it a hockey stick.

So, what changed? Here are some thoughts and hypotheses:

- Guidelines changed a little. We can see in the data that Freddie did almost zero PIWs on cash out loans, but in May that changed, and at lease for LTVS below 70%, they did almost 15,000 cash out loans with no appraisal.

- AVMs changed. Back when PIWs were introduced, AVMs operated in a +/- 10% paradigm. They were more concerned with hit rates than anything else, and they worked best on track homes. But, today they are operating in a +/- 4% world, hit rates are great, and cascades allow lenders to pick the AVM that’s most accurate for the application.

- Borrowers changed. These days, borrowers have grown up with online tools that give them answers. They are more likely to read about their symptoms on WebMD before going to the doctor, and they are more likely to look their home up on Zillow before calling their realtor. In the past, if home was purchased with a low LTV, who was it that required an appraisal? Typically, it was borrowers that wanted the appraisal – more as a safety blanket than anything else. They wanted reassurance that they were not getting ripped off. Today, for some people, Zillow can provide that reassurance without the $500 expense.

- Lenders changed. You would think that they are nimble and adaptable to new opportunities. But where the rubber meets the road, it’s still people talking to customers, and underwriters signing off on loans. If loan officers aren’t aware of the guidelines, they’ll just order an appraisal. Often ordering an appraisal, because it can take so long, is just about one of the first things done in the process, regardless of whether it’s necessary. After all, it’s usually necessary, and it takes SO long (relatively speaking, of course). I have known lenders who required their loan officers to collect money for an appraisal to demonstrate customer commitment. But, lenders are starting to incorporate PIWs into their processes and take advantage of those opportunities to present a loan option with $500 less in costs.

Accurate AVMs are a necessary but not sufficient criteria for PIWs, and now that AVMs are much more accurate, PIWs are much more practical, and we’re seeing much higher adoption.

So now what should we expect going forward? The trend will likely continue. There’s a lot of room left in some of those categories for PIWs to grab a larger share.

If agencies are doing it, everyone else will. If there are lenders not using PIWs to the extent possible, they are going to be at a disadvantage.

Black Knight’s Cascade Improved

Black Knight just announced an addition to its ValuEdge Cascade. It will now include the CA Value AVM, developed by Collateral Analytics, which recently became a Black Knight company.

AVMetrics helped with the process, doing the independent testing used to optimize the cascade performance. Read more about it in their press release.

Four Points to Consider Before Outsourcing AVM Validation

AVMs are not only fairly accurate, they are also affordable and easy to use. Unfortunately, using them in a “compliant” fashion is not as easy. Regulatory Bulletins OCC 2010-42 and OCC 2011-12 describe a lot of requirements that can be challenging for a regional or community institution:

- ongoing independent testing and validation and documentation of testing;

- understanding each AVM model’s conceptual and methodological soundness;

- documenting policies and procedures that define how to use AVMs and when not to use AVMs;

- establishing targets for accuracy and tolerances for acceptable discrepancies.

The extent to which these requirements are applied by your regulator is most likely proportional to the extent to which AVMs are used within your organization; if AVMs are used extensively, regulatory oversight will likely demand much tighter adherence to the requirements as well as much more comprehensive policies and procedures.

Although compliance itself is not a function that can be outsourced (it is the sole responsibility of the institution), elements of the regulatory requirements can be effectively handled outside the organization through outsourcing. As an example, the first bullet point, “ongoing independent testing and validation and documentation of testing,” requires resources with the competencies and influences to effectively challenge AVM models. In addition, the “independent” aspect is challenging to accomplish unless a separate department within the institution is established that does not report up through the product and/or procurement verticals (e.g. similar to Audit, or Model Risk Management, etc.). Whether your institution is a heavy AVM user or not, the good news is that finding the right third-party to outsource to will facilitate all of the bullet points above:

- documentation is included as part of an independent testing and validation process and it can be incorporated into your policies and procedures;

- the results of the testing will help you shape your understanding of where and when AVMs can and cannot be used;

- the results of the testing will inform your decisions regarding the accuracy and performance thresholds that fit within your institution’s risk appetite. In addition,

- an outsourced specialist may also be able to provide various levels of consultation assistance in areas where you may not have the internal expertise.

Before deciding whether outsourcing makes sense for you, here are some potential considerations. If you can answer “no” to all of these questions, then outsourcing might be a good option, especially if you don’t have an independent Analytics unit in-house that has the resource bandwidth to accommodate the AVM testing and validation processes:

- Is this process strategically critical? I.e., does your validation of AVMs benefit you competitively in a tangible way?

- If your validation of AVMs is inadequate, can this substantially affect your reputation or your position within the marketplace?

- Is outsourcing impractical for any reason? I.e., are there other business functions that preclude separating the validation process?

- Does your institution have the same data availability and economies of scale as a specialist?

The Way Forward

Here are some suggestions on how to go about preparing yourself for selecting your outsource partner:

- Specify what you need outsourced. If you already have Policies and Procedures documented and processes in place, there may be no need to look for that capability, but there will necessarily still be the need to incorporate any testing and validation results into your existing policies and procedures. If you have previously done extensive evaluations of the AVMs that you use, in terms of their models’ conceptual soundness and outcomes analysis, there’s no need to contract for that, either. See our article on Regulatory Oversight to get some ideas about those requirements.

- Identify possible partners, such as AVMetrics, and evaluate their fit. Here’s what to look for:

- Expertise. It’s a technical job, requiring a fair amount of analysis and a tremendous amount of knowledge about regulatory requirements in general, and specifically knowledge relative to AVMs; check the résumés of the experts with whom you plan to partner.

- Independence. A vendor who also sells, builds, resells, uses or advocates for certain AVMs may be biased (or may appear to be biased) in auditing them; validation must be able to “effectively challenge” the models being tested.

- Track record. Stable partners are better, and a long term relationship lowers the cost of outsourcing; so look for a partner with a successful track record in performing AVM validations.

- Open up conversations with potential partners early because the process can take months, particularly if policies and procedures need to be developed; although validations can be successfully completed in a matter of days, that is not the norm.

- Make sure your staff has enough familiarity with the regulatory requirements so as to be able to oversee the vendor’s work; remember that the responsibility for compliance is ultimately on you. Make sure the vendor’s process and results are clearly and comprehensively documented and then ensure that Internal Audit and Compliance are part of that oversight. “Outsource” doesn’t mean “forget about it;” thorough and complete understanding and documentation is part of the requirements.

- Have a plan for ongoing compliance, whether it is to transition to internal resources or to retain vendors indefinitely. Set expectations for the frequency of the validation process, which regulations require to be at least annually or more often, commensurate with the extent of your AVM usage.

In Conclusion

AVM testing and validation is only one component in your overall Valuation and evaluation program. Unlike Appraisals and some other forms of collateral valuation, AVMs, by their nature as a quantitative predictive model, lend themselves to just the type of statistically-based outcomes analysis the regulators set forth. Recognizing this, elements of the requirements can be an outsourced process, but it must be a compliment to enterprise-wide policies and practices around the permissible, safe and prudent use of valuation tools and technologies.

The process of validating and documenting AVMs may seem daunting at first, but for the past 10 years AVMetrics has been providing ease-of-mind for our customers, whether as the sole source of an outsourced testing and validation process (that tests every commercial AVM four times a year), or as a partner in transitioning the process in-house. Our experience, professional resources and depth of data have enabled us to standardize much of the processing while still providing the customization every institution needs. And probably one of the most critical boxes you can check off when outsourcing with AVMetrics is the very large one that requires independence. It also bears mentioning that having been around as long as we have, our customers have generally all been through at least one round of regulatory scrutiny, and the AVMetrics process has always passed regulatory muster. Regulatory reviews already present enough of a challenge, so having a partner with established credentials is critical for a smooth process.