The Era of Full Steam Ahead!

Six months before the pandemic, we published an article on the outlook for regulation related to AVMs. At the time, we identified three trends.

- The administration was encouraging more use of AVMs (e.g., via hybrids), and tempering that with calls for close monitoring of AVMs.

- The de minimis threshold change foreshadowed an increase in reliance on AVMs in some lower value mortgages.

- The Appraisal Subcommittee summit was focused on standardization across agencies and alternative valuation products, namely, AVMs. Conversation focused on quality and risk as well as speed.

We saw those trends pointing to increased AVM use balanced by a focus on risk, quality and efficiency.

Sure enough, the following events unfolded:

- The de minimis threshold was indeed raised, right before the pandemic changed everything.

- The appraisal business was turned upside down for a period during the pandemic.

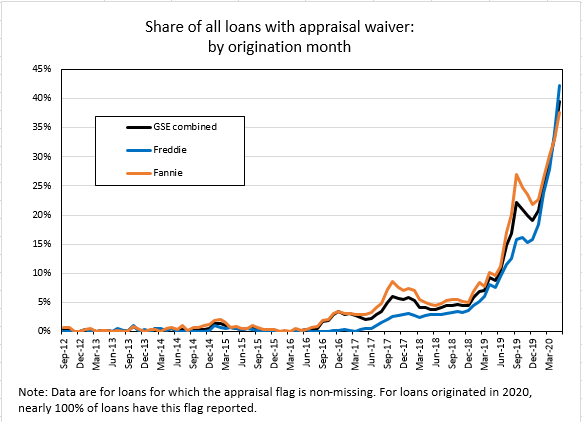

- Property Inspection Waivers (PIWs) took off in a big way as Fannie and Freddie skipped appraisals on a huge percentages of their originations (up to 40% at times).

Halt! About Face!

And then the new administration changed the focus entirely. No longer were the conversations about speed, efficiency, quality, risk and appraisers being focused on their highest and best use. Instead, conversations focused on bias.

Fannie produced a report on bias in appraisals. CFPB began moving on new AVM guidelines and proposed using the “fifth factor” to measure Fair Lending implications for AVMs. Congress held committee hearings on AVM bias.

New Direction

Then The Appraisal Foundation’s Industry Advisory Council produced an AVM Task Force Report. Two of AVMetrics’ staff participated on the task force and helped present its findings recently in Washington D.C.

The Task Force made specific recommendations, but first it helped educate regulators about the AVM industry.

One specific recommendation was to consider certification for AVMs. Another was to use the same USPAP framework for the oversight of AVMs as is used for the oversight of appraisals. It’s all laid out in the AVM Task Force Report.

Taking It All In

Our assessment three years ago was eerily accurate for the subsequent two years. Even the unexpected pandemic generally moved things in the direction that we were pointing to: increased use of AVMs through hybrids.

What we failed to anticipate back then was a complete change in direction with the new administration, and maybe that’s to be expected. It’s hard to see around the corner to a new administration, with new personnel, priorities and policy objectives.

The Task Force Report provides some very practical direction for regulations. But the recent emphasis on fair lending, which emerged after the Task Force began meeting and forming its recommendations, could influence the direction of things. The end result is a combination of more clarity and, at the same time, new uncertainty.