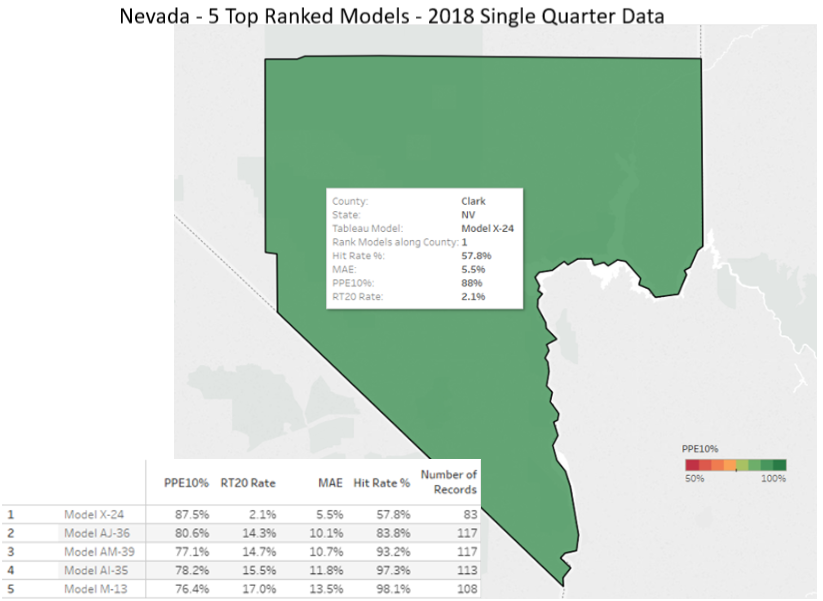

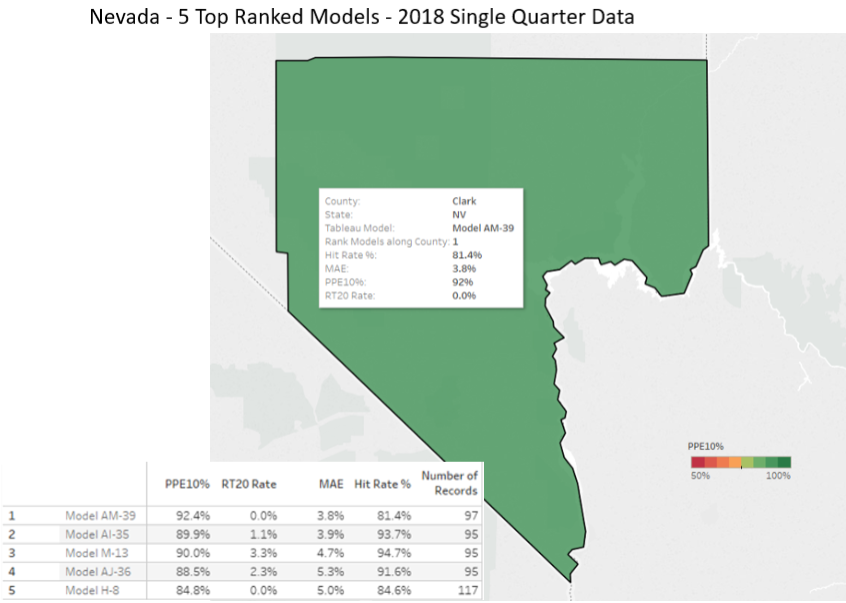

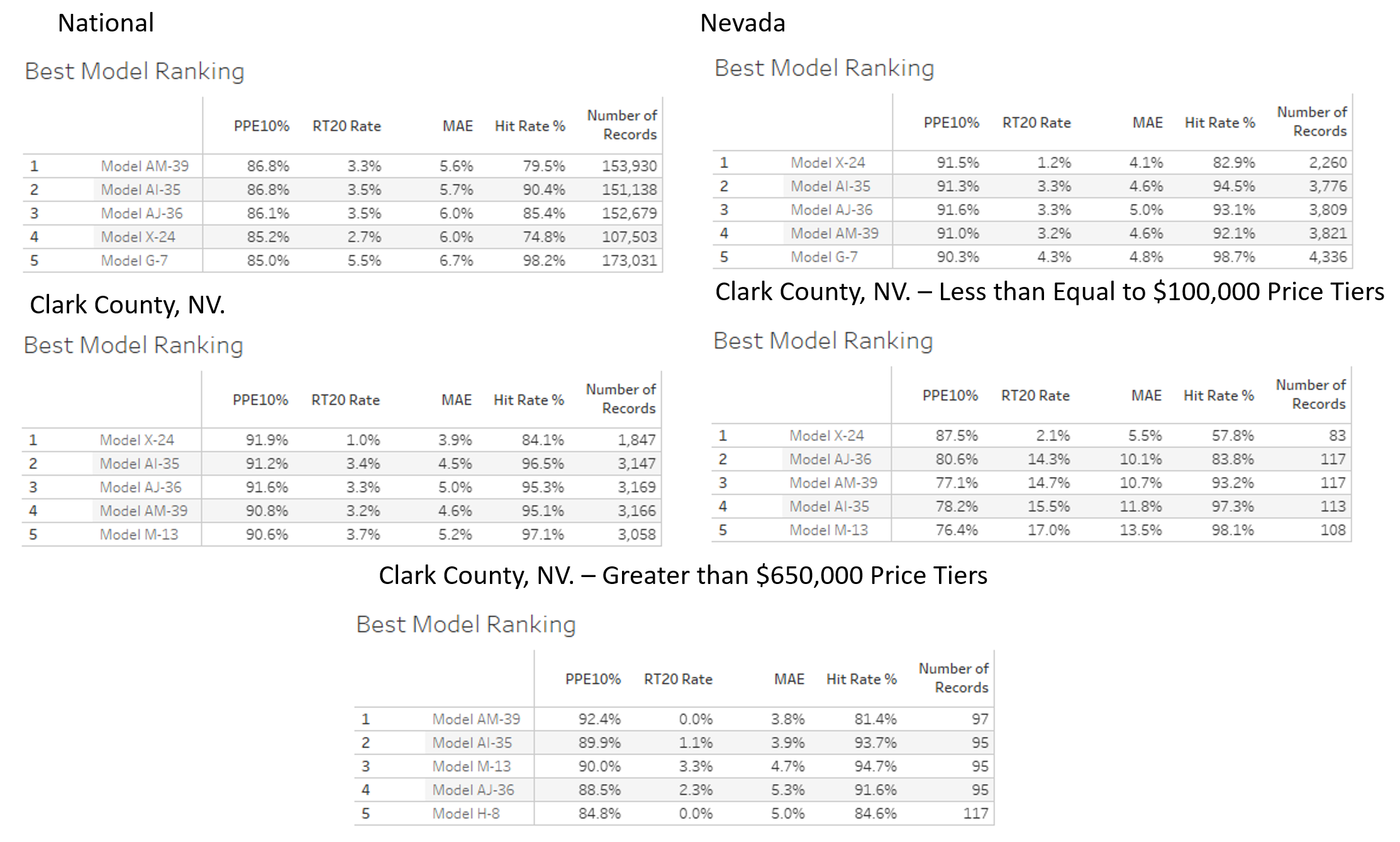

As always, changes are coming to the valuation industry. These changes have been germinating in government and industry for a long time, but they’ve made progress in the last year, and I believe that they’re likely to emerge sometime this year. I expect that we may see more regulatory changes liberalizing the use of AVMs soon.

I think that you’ll come to that same conclusion, too, if I share a couple milestones that I’ve observed and put them together with some insights I’ve gathered from talking to industry leaders.

The first milestone I will highlight was the July 2018 Financial System report by Secretary Mnuchin, which is consistent with the administration’s new attitude towards regulation. The report is far-reaching, and it includes thoughtful commentary about the uses of AVMs (see, for example, page 103-106). It recommends updating FIRREA appraisal requirements to accommodate increased usage of AVMs and hybrids. It also advocates for increased monitoring of AVMs and the application of rigorous market standards. And, it recommends focusing the use of AVMs and hybrids on loan programs with other mitigating risk factors.

The next milestone I will highlight was the proposed change in the de minimis threshold that was put out for comment in November of last year. The change would raise the threshold below which a residential mortgage could be originated with an evaluation, utilizing an AVM in lieu of a traditional appraisal. It would be raised from $250,000 to $400,000.

To those milestones I would add a third data point. Last November I attended the Appraisal Subcommittee roundtable entitled: “The Evolving Real Estate Valuation Landscape.” As part of the of the Federal Financial Institutions Examination Council, the roundtable brought together industry representatives and government officials (see the table below) to discuss real estate valuation.

The day was split into two sessions; the morning and afternoon sessions each began with a panel of industry experts who addressed a series of prepared questions. In addition, there was a roundtable discussion focused on quotes from the July 2018 Financial System report referenced above.

The topic for the morning discussion was “Harmonizing Real Estate Valuation Requirements Across the Federal Government.” This session focused on identifying various federal appraisal statutory and regulatory requirements and exploring opportunities to harmonize those requirements, e.g., VA, FHA, and FHFA all having differing valuation requirements and standards.

The afternoon panel discussion topic was; “The Evolution of Real Estate Valuation” which focused on evolving valuation needs in commercial and mortgage lending. A key area of this session was focused on Alternative Valuation Products inclusive of AVM’s and their increasing used by lenders and the secondary market.

The roundtable discussion started with quotes about AVMs and hybrid valuation products and focused on standards. The group also contemplated how alternative valuation techniques can impact quality and mitigate risk. Finally, one quote that focused on speeding the adoption of technology was discussed.

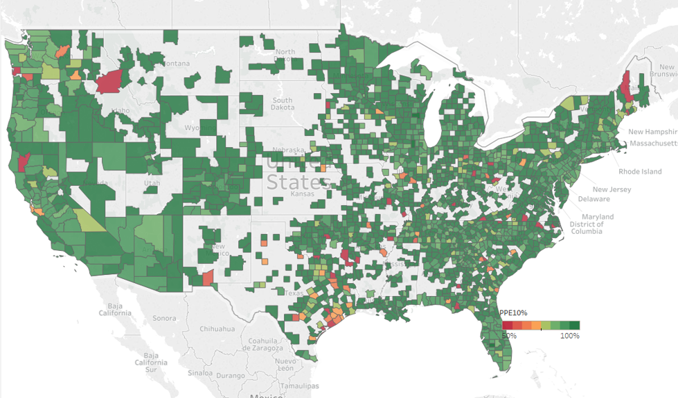

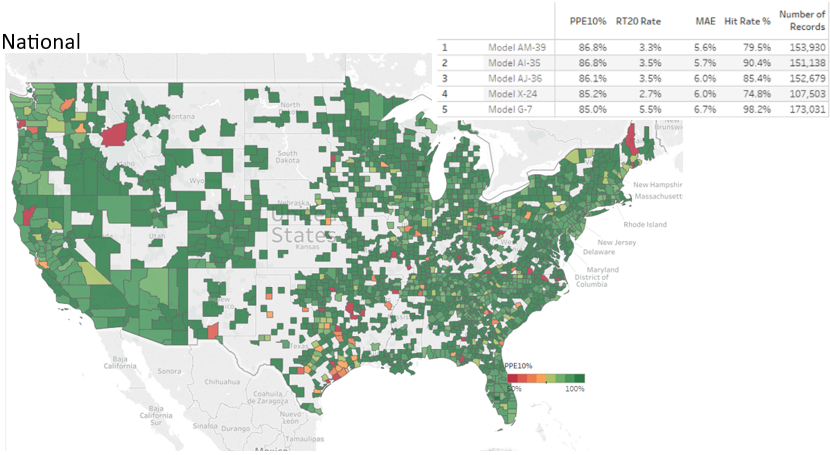

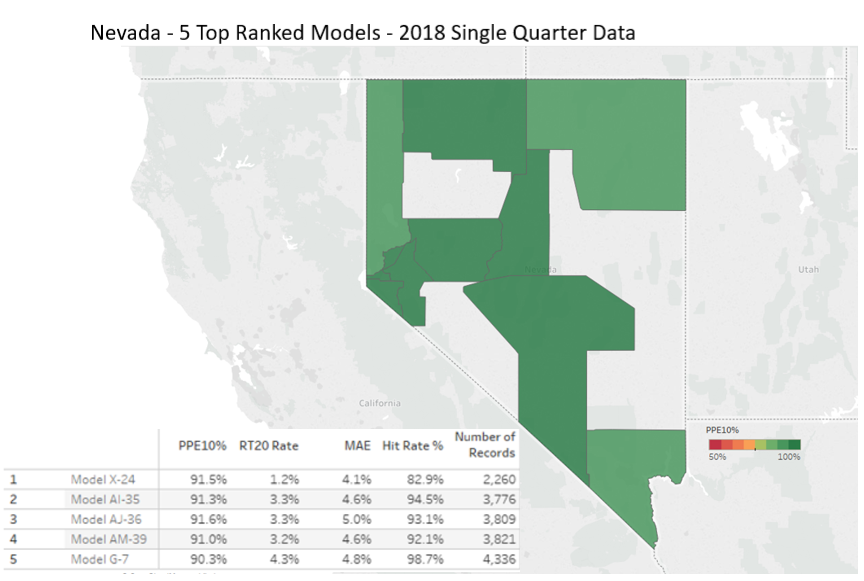

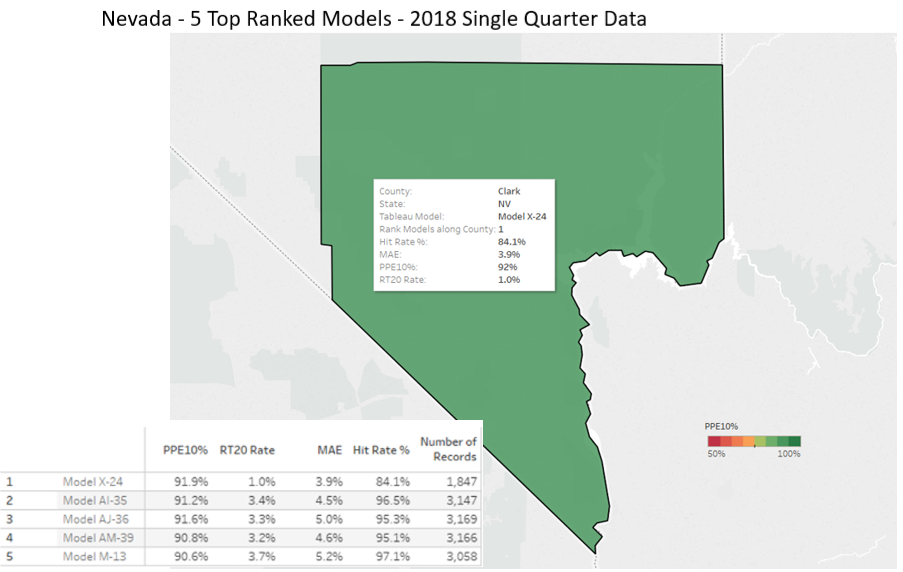

As I write this six months later, I see the pieces of the puzzle coming together. Obviously, there is momentum behind the increased usage of AVMs, for their independence, increasing accuracy, speed and efficiency. But there is also an implicit concern to avoid opening the door to more risk. I see this being expressed by talk about “standards,” alternative products, such as “hybrids” and increased monitoring.

As I have written elsewhere, I welcome changes that make better use of our valuable and limited resources, namely the appraisers themselves. As AVM quality improves and the number of appraisers shrinks, we should encourage appraisers to be focused on their highest and best use. Their expertise should be focused on the complex, qualitative aspects of property valuation such as the property condition and market and locational influences. They should also be focused on performing complex valuation assignments in non-homogeneous markets. Trying to be a “manual AVM” is not the highest and best use of a highly qualified appraiser, and I expect that Treasury, the FDIC and legislators are moving in this same direction.

Lee Kennedy

| Participants in “The Evolving Real Estate Valuation Landscape” Appraisal Subcommittee, Federal Financial Institutions Examination Council, 2018 | ||

| Government | Trade Organizations | Industry Participants |

| The Appraisal Foundation (TAF) | American Bankers Association | AVMetrics, LLC |

| Association of Appraiser Regulatory Officials (AARO) | American Society of Appraisers | Bank of America |

| Consumer Financial Protection Bureau (4) | American Society of Farm Managers and Rural Appraisers | Clarocity Valuation Services |

| Federal Deposit Insurance Corporation(3) | Appraisal Institute | ClearBox |

| Federal Housing Finance Agency(4) | Homeownership Preservation Foundation | CoreLogic |

| Federal Reserve Board(5) | Independent Community Bankers of America | Cushman & Wakefield Global Services, Inc. |

| Freddie Mac | Mortgage Bankers Association | Farm Credit Mid-America |

| Internal Revenue Service | National Association of Home Builders | First American Mortgage Solutions |

| National Credit Union Administration | National Association of Realtors | Genworth Financial |

| Office of the Comptroller of the Currency (4) | Real Estate Valuation Advocacy Association (REVAA) | JPMorgan Chase & Company |

| Tennessee Real Estate Appraisers Commission | State appraiser coalitions representative | Old Line Bank |

| Texas Appraiser Licensing and Certification Board | Quicken Loans | |

| U.S. Department of Agriculture | ServiceLink | |

| U.S. Department of Justice (2) | ||

| U.S. Department of the Interior (2) | ||

| U.S. Department of Veterans Affairs | ||

| US. Department of Housing and Urban Development |